With their significant part in the supply chain through maintaining inventory of cars awaiting sale, dealerships were able to increase vehicle prices — and their profit margins. The study found these markups to be a prime driver behind new-vehicle inflation for consumers over the past three years.

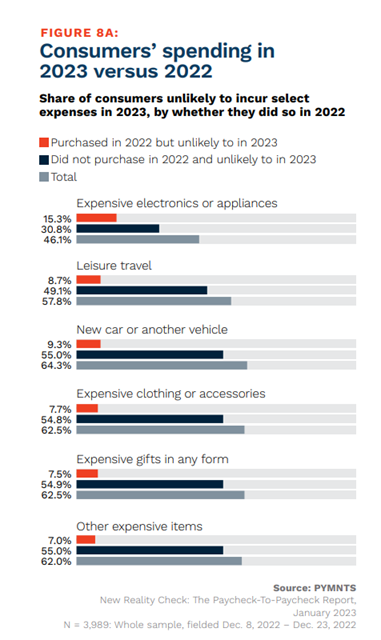

The dealer-driven markups are perhaps partially the reason why 64% of consumers say they are unlikely to purchase a car in 2023, per the January PYMNTS collaboration with LendingClub, “New Reality Check: The Paycheck-To-Paycheck Report.”

Cars were cited by more consumers as unlikely to be purchased than any other large expense we tracked, including leisure travel, gifts and luxury clothing.

Supply chain issues leading to certain limited inventory were almost certainly a factor in 2022’s price tags and possibly corresponding car sales numbers. Last year, just 13.7 million auto purchases occurred, the lowest mark in more than a decade, as manufacturers navigated chip shortages and logistics challenges. Shortages in which the vehicles shoppers are seeking may be unavailable and higher prices are each potential reasons behind consumers’ continued purchasing hesitancy into 2023.

This purchasing hesitancy has extended into used car sales, where AutoNation reported revenue down 21% in the first quarter of 2023 compared to the same period the previous year, representing a decrease of $540 million. The dealer has shifted focus from selling to service and customer-relationship building and was partially the reason behind AutoNation’s January acquisition of RepairSmith. The full-service mobile automotive repair and maintenance solution, based in Los Angeles, has a major presence in the western U.S.

Advertisement: Scroll to Continue

Suffering used car sales led to an April 3% drop in consumer-facing prices, after increasing 8.6% over Q1 2023. The number of used vehicles sold also declined 8% in April, both month over month and year over year.

Higher prices are almost certainly a factor in consumers’ outstanding loan size, rising from $1.44 trillion in Q3 2021 to $1.52 trillion in Q3 2022. This has led banks and lenders to voice concerns about buyers’ debt load during recent earnings calls. Wells Fargo’s auto segment earnings were down in March year over year, to $392 million, with its auto loan originations down 32% year over year to $5 billion. JPMorgan’s auto loans and leased assets were $80.3 billion in March, down from $85.7 billion during the same quarter the previous year. The banking giant’s net charge-off rate for the segment was 0.4% during the period, up from 0.2% last year. Their 30-day-plus delinquency rate was up to 0.9% from last year’s 0.6%.

Auto sales are slumping due to multiple factors for which dealers may be responsible, including budget-busting price tags and a lack of available inventory due to macroeconomic pressures. No matter the cause, just as with other retail sectors, it may be a while longer before car merchants and manufacturers see a return to economic “normal.”