In retail, get ready for the “big reconsideration.”

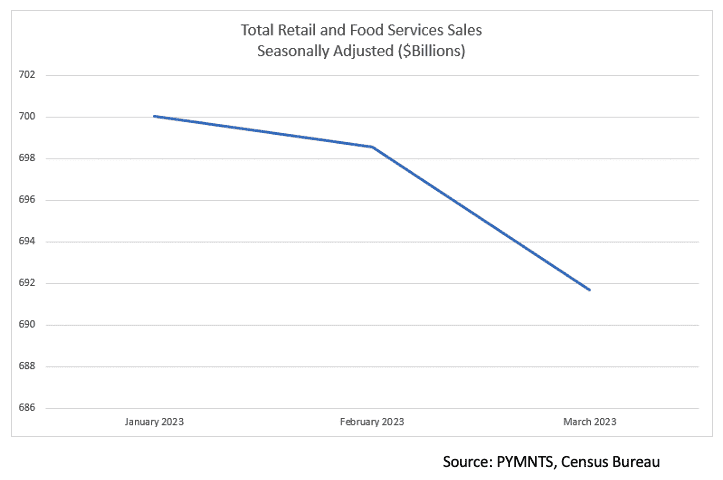

The latest retail sales data released Friday (April 14) show that in March — and for the second straight month — consumers pulled back their spending.

Overall, the data from the U.S. Census Bureau shows that spending declined 1% month over month on a seasonally adjusted basis. That follows a 0.2% decline seen in February versus January.

Consumers are throttling back on the levers they have in place to conserve at least some financial firepower.

It makes sense that in a few key categories, there’s a re-examination of what consumers and households need to have versus what they’d like to have. And when there’s a recalibration of those categories, there’s a mindset that some things can wait.

So seems to be the case with some key categories of retail spending, where price tags can be significant, but at least some of these goods are long-lasting enough so that what we’ve got in hand is good enough for now.

No Upgrades — Not Now, at Least

Replacements or upgrades? Well, they can wait for another day.

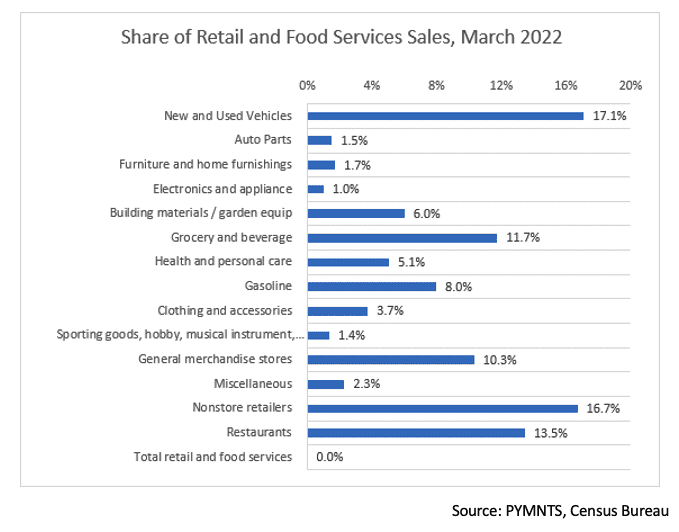

Spending on electronics and appliances was down 2.1% month over month and down by 10.3% year on year. Furniture and home furnishings were down a respective 1.2% and 2.4%. Spending at clothing and accessories stores slipped 1.7% month on month and 1.8% from a year ago. At automobile/vehicle dealers, spending was 1.5% lower month on month and by 0.3% as measured against March 2022. The categories are a relatively smaller portion of overall retail sales. Much depends on the ticket size, which is why vehicles have a mid-teens percentage contribution; clothes and accessories are a bit less than 4%.

The March retail sales report dovetails with PYMNTS’ data that shows, in the aggregate, a roughly $8 billion cut to retail spending in just the past few months.

Other PYMNTS research shows that 67% of retail customers expect significant price increases in the next 12 months. The average consumer does not expect inflation to return to normal until the end of 2024.

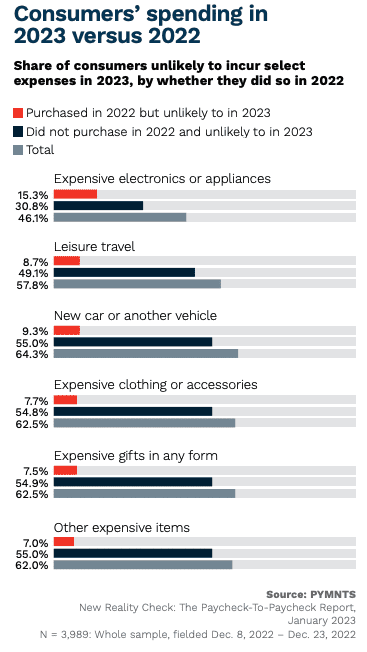

The pullback was presaged at the beginning of the year in PYMNTS’ “Economic Outlook and Sentiment” report. A total of about 46% of consumers are unlikely to buy expensive electronics this year (whether they did so or not last year). That metric widens to about two-thirds in categories such as cars or expensive clothing.

The read-across here is that with the first quarter under our collective belts, the pressure is going to be on retailers that have banked on the willingness of consumers to spend significantly to look their best, have the latest gadgetry in hand, or sit behind the newest wheel.

J.P. Morgan’s earnings results, released Friday morning, showed that credit and debit spending was up double-digit percentage points in the March quarter. But the spending, in PYMNTS’ data, is being shifted toward the everyday essentials that have become more expensive along with everything else. The luxury goods that have satisfied the urge to splurge may have to wait a while.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More