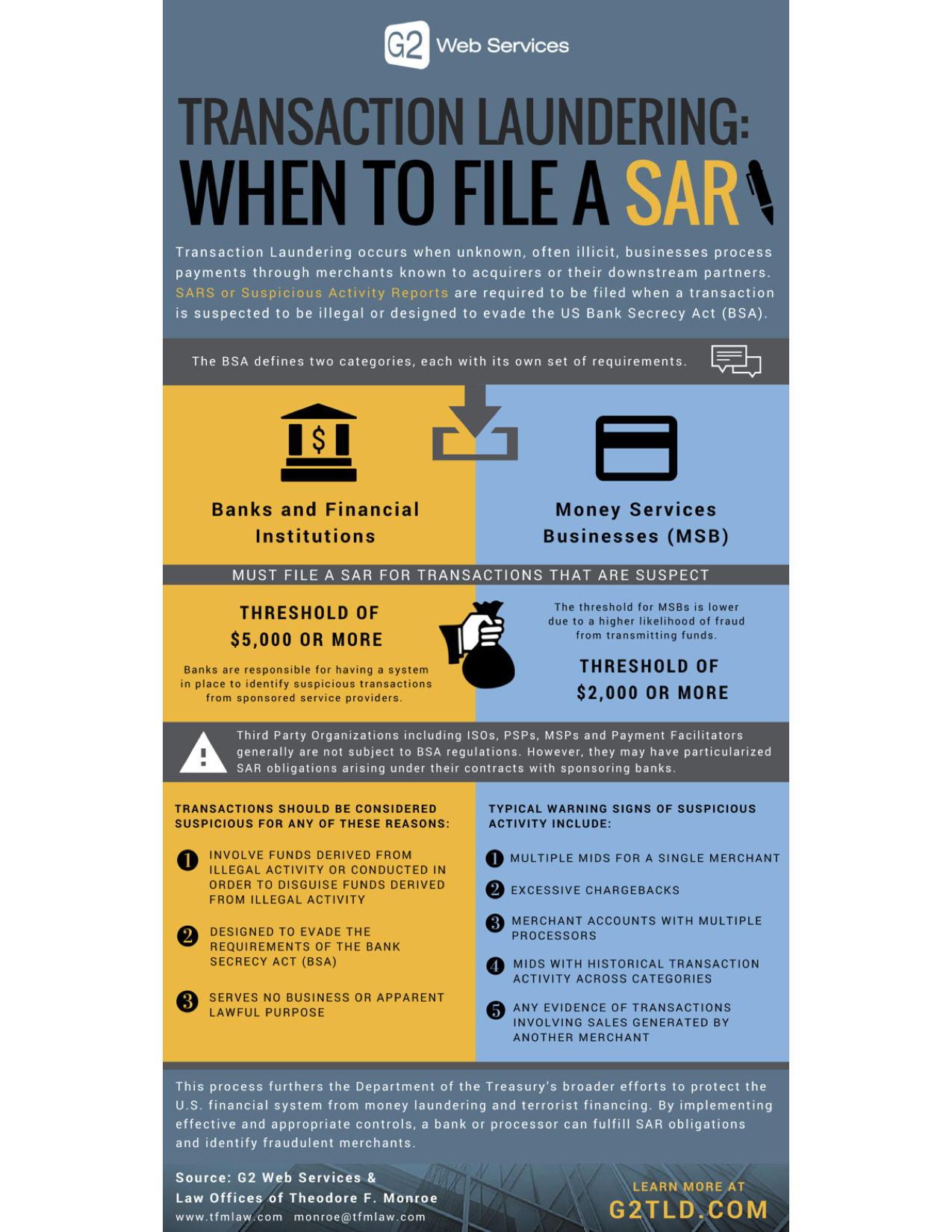

According to the post, authored by Theodore F. Monroe and Bradley O. Cebeci of the Law Offices of Theodore F. Monroe, which specializes in payment processing, SAR makes up the cornerstone of the Bank Secrecy Act (BSA) reporting system.

Under federal regulations, banks and financial institutions are required to file a SAR if they have any reason to believe financial crimes and transactions conducted or attempted through them may involve potential money laundering or other illegal activity.

Interestingly enough, certain Money Services Businesses (MSB), non-bank third-party organizations, such as ISOs/MSPs, payment facilitators/payment service providers, data processors and network providers (collectively known as “TPOs”) are not typically subject to adhere to BSA requirements.

“Thus, it is the acquiring bank’s responsibility to (1) ensure that a TPO’s incident reporting and management program contains clearly documented processes and accountability for identifying, reporting, investigating and escalating incidents of credit card laundering and other suspicious activity; and (2) monitor TPO compliance and processing information on an ongoing basis to ensure compliance with the acquirer’s SAR obligations,” Monroe and Cebeci explained in the post.

A bank may increase its risk of suspicious activity taking place if it’s unable to accurately identify and understand the nature and sources of the transactions conducted or attempted by, at or through them. The post added that, when banks and financial institutions do not have an adequate program in place for monitoring and addressing their third-party relationship risks, they may be subject to regulatory intervention.

Advertisement: Scroll to Continue

To learn more about who, when and why to file a SAR per the Bank Secrecy Act, please see the infographic below: