Payments fraud is not just a matter of end user vulnerability — the unwitting consumer who clicks on a link or the authorized push payment that disappears into the proverbial ether after a fraudster impersonates a family member or friend via text message.

Payments fraud is not simply a matter of regulation, where the “right” rules, or simply “more” rules, will build an insurmountable wall of defense against bad actors.

Now, more than ever, the rise of online commerce and card not present transactions spotlights the fact that fraud preys on the vulnerabilities of money mobility itself.

In the digital age, we all want funds to move from an account to any account regardless of who the payer or payee might be — and often those funds move across a range of financial institutions and payment instruments as varied as cash, checks and digital wallets.

The weaknesses to be found with the fraud controls surrounding money “into” the system are paramount.

To that end, and as reported in Ars Technica, online fraudsters have gotten ever-bolder, with card-testing and other schemes on the rise. The site detailed one example of a wave of fraud enacted against a small Kansas-based firm, inundated by “card testing.” And in that case, the online fraudsters used purchases on merchants’ sites, some of them as small as a few cents, to test the validity of debit card numbers.

The article spotlights Ally Bank, but the problem is endemic to the financial services arena at large. And not surprisingly, call centers are swamped with calls by consumers alarmed and distressed by the charges — waiting on hold for hours to be helped.

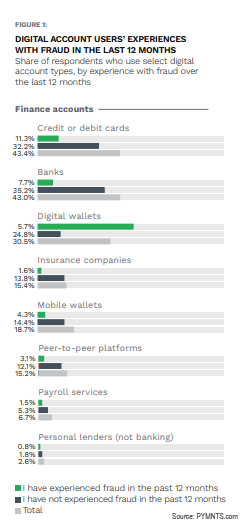

PYMNTS’ own data shows that cards are indeed the favorite target of fraudsters, at least for the moment, where 11% of consumers surveyed said they’d experienced fraud in the past 12 months.

As many as 29% of people surveyed have said they’d be inclined to switch banks if they felt that fraud incidents had been poorly handled by their financial institution (FI). All of this puts the onus on FIs to leverage fraud detection technology that also has better decisioning built in to enable money mobility that is safe right at the “money in” stage.

Read Also: PYMNTS Intelligence: Fighting Fraud While Ensuring Money Mobility

In one recent PYMNTS interview, PYMNTS’ Karen Webster spoke with Ingo Money Executive Vice President and Chief Product Officer Lisa McFarland and Senior Vice President of Payments Dennis Mullin. And in that discussion, the executives took note of the complexity of connections — the nuts and bolts of enabling money to be moved anywhere, where inbound funds can be received from any accounts.

Read More: Complex Money Mobility Made Easier With Smart Partners and Strong Platforms

Ingo Money CEO Drew Edwards has spotlighted in this space that account issuance has been hampered in the past by the specter of fraud, where FIs and FinTechs have limited issuers’ ability to offer accounts to the entirety of their consumer bases. In just one example check services might conceivably be made available to direct deposit customers who have been through at least two pay cycles with the FI. That demographic tends to be less than 30% to 40% of the account base, Edwards said in a recent interview.

In detailing how advanced tech can strengthen money mobility at the point of initial contact and by extension can widen financial services access for the population at large, in May, Ingo Money announced the availability of its Inbound Digital Transfer and Risk Services.

The service uses device-related attributes spanning the location in which a transaction is happening, the consumer’s behavior when they’re interacting with the site or the app, and account-related details to stop fraud risk at the initial moments of engagement with the FI or FinTech.

The decisioning at the moment of account funding may be among the best lines of defense against fraud that, after all, cannot damage financial services if it cannot gain access to the ecosystem in the first place.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More