Once upon a time, or at least a few decades back, consumers didn’t have much say in their financial institutions’ fraud-fighting innovations.

With only a few retail banks to choose from, they had to accept whatever systems their FIs put in place to secure customer funds, or switch to a competitor who at the time likely had similar offerings. However, with the advent of neobanks and other FinTech competitors, times have changed.

Consumers now are more security-savvy than ever, especially those of digital-native generations, who seek more empowerment over their finances and want a say in how that money and personal information are protected. They are also unafraid to voice their preferences — and take their business elsewhere if their needs go unmet.

PYMNTS’ latest collaboration with Entersekt, “Visible and Invisible Security: Perceptions in Digital Banking,” details customer choice when it comes to fraud-fighting measures.

The ratio of consumers comfortable with current security measures may be of concern to traditional banks or other FIs relying on their reputation for trust to keep customers coming. Approximately half of customers overall are concerned about the safeguards their FI has in place to protect their money. This fear isn’t without merit, as 62% of big banks deal with crime increases. It also means a possible chance of those customers moving their deposits to places where they feel are more secure — be it a neobank or other competitor. FIs putting effort into their retention strategies may consider renewed investments into their fraud-fighting tools as part of that plan.

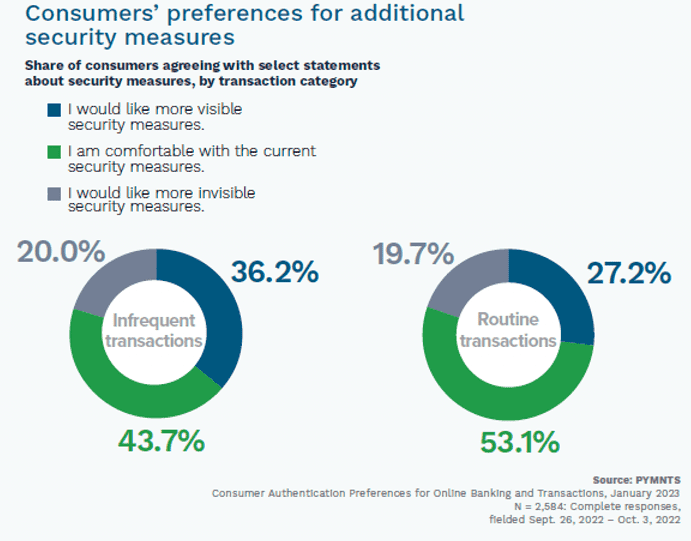

As preference for proactivity leans toward more visible security measures over invisible in both infrequent and routine transactions, FIs may consider concentrating their efforts on demonstrable innovations first. Those include tools such as password modernization, multifactor authentication and biometrics.

If FIs have the means and budget, they certainly have the possibility of creating all or some of these tools in-house. Other innovations may be found in a third-party partnership or complete outsourcing.

Making passwordless authentication a reality are companies such as Prove Identity, whose stable of FI-focused products includes layered digital multifactor authentication tools. Its newest effort in authentication modernization involves essentially embedding authentication passively into digital experiences via the cryptographic key (i.e., SIM card) in every mobile device.

On the biometrics end of authentication innovations, companies such as IDEX are providing solutions for FIs both in the U.S. and overseas. In November, Italian banking firm Sella Group began offering a new payment card to select target segments, powered by IDEX’s Biometrics TrustedBio fingerprint sensor solution. The Sella Group launch was preceded by IDEX’s debuting of a full-scale biometric payment card program in the Middle East through a major regional bank.

In today’s digital-leaning age — where every customer acquisition counts — bank customer service is long past simply service with a smile. Listening to consumer preference when it comes to security they can see, among other services, may be the new retention baseline for FIs that otherwise risk losing customers to more trusted competitors.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More