Credit card fraud is a rising concern for American consumers, with nearly 1 in 3 reporting fraudulent charges in the past year. As incidents of fraud increase, so does consumer anxiety, with 37% of individuals expressing heightened worry.

A PYMNTS Intelligence report, “Credit Card Fears Can Drive Consumers to Switch Banks,” in collaboration with i2c, reveals insights about how fraud affects consumer behavior, their expectations of banks, and how financial institutions must act to retain customer trust.

The scope of credit card fraud is widespread, with 28% of consumers reporting they have been victims in the last year. Millennials are particularly affected, with 33% of this demographic experiencing fraud, a statistic that highlights the financial vulnerability of younger consumers.

High-income earners, often with multiple cards, are also at risk, with 33% of individuals earning over $100,000 reporting fraud incidents. Meanwhile, Generation Z, while affected by fraud, is less likely to hold credit cards in the first place, making up 31% of victims.

These statistics underscore the anxiety around fraud, particularly among groups like millennials and individuals living paycheck to paycheck. Among the latter, 43% expressed extreme concern about the threat of fraud. This highlights a crucial point: the more financially stretched consumers are, the more fragile their trust becomes when fraud occurs.

Consumers expect banks to be the first line of defense against fraud. Consider 91% of consumers report their banks intervened when fraud was detected, often before the consumer even realized it. For instance, 28% learned of fraudulent charges only through mobile notifications, while 26% discovered it on their bank statements.

The importance of intervention relates to customer service and maintaining customer satisfaction. Consumers whose banks detected fraud were notably more satisfied with the outcome. According to the report, 90% of victims whose banks took immediate action were “very” or “extremely” satisfied with how the situation was managed, compared to 50% of those who discovered fraud independently.

Banks that fail to act quickly risk losing customer trust and loyalty. Consumers who experience delays in fraud detection may lose confidence in their bank, with some even switching institutions if the response is inadequate.

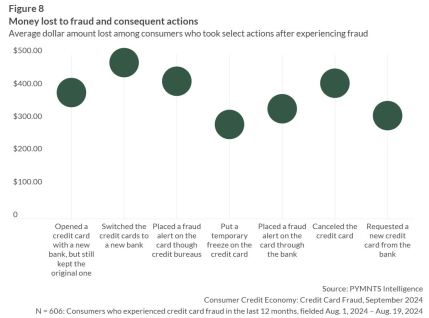

The consequences of credit card fraud go beyond financial losses; they can also drive consumers to switch banks. While the most common action taken by victims is requesting a new card from the same bank (42%), a smaller number of consumers take more drastic measures, such as canceling their cards (17%) or switching banks entirely (5.2%).

The financial implications are significant for those who switch. On average, consumers who changed banks lost $475 due to fraud, compared to the $287 lost by those who froze their cards.

Consumers who are already highly concerned about fraud are more likely to take drastic actions. For example, 23% of those who are “very” or “extremely” worried about fraud would consider switching banks if they experienced fraud, underscoring the need for banks to respond quickly and take measures that reduce fraud risk.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More