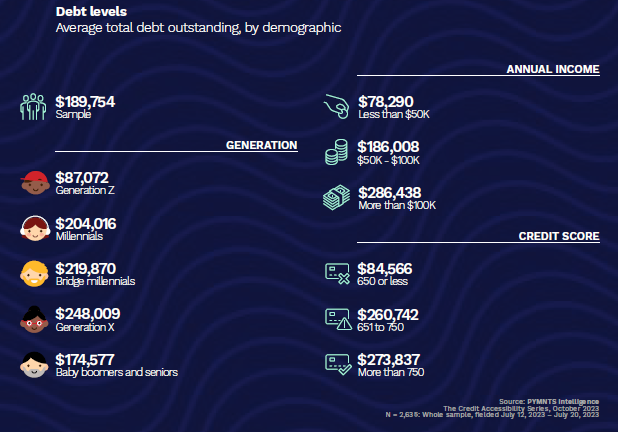

Current economic conditions and consumers’ drive to maintain a certain standard of living has led to a pervasive level of private debt across the economy, with 1 in 3 U.S. consumers owing more than $250,000 in outstanding debt, mostly made up by mortgages and auto loans.

This is one of the key findings detailed in “The Credit Accessibility Series: Economic Malaise Exacerbating U.S. Consumer Debt Levels,” a PYMNTS Intelligence and Sezzle collaboration, which explores how high levels of debt impact different consumers’ credit accessibility, livelihoods and purchasing power.

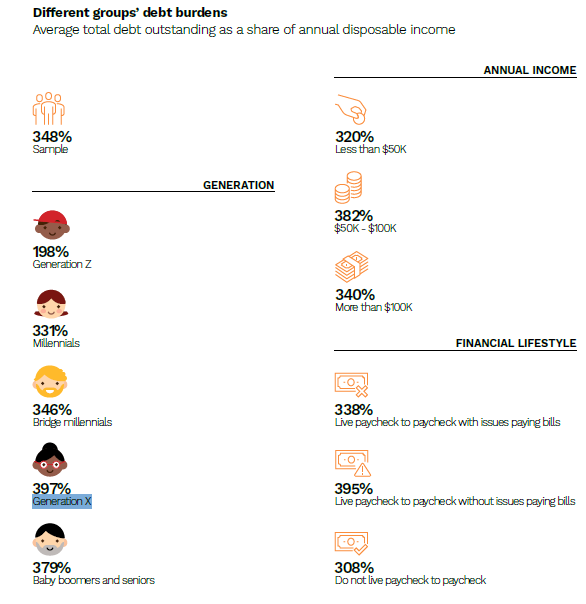

Drilling down into the data shows that Generation X, the age group born between the early 1960s and early 1980s, owe the most, both in absolute terms as well as relative to their disposable income. Their average outstanding debt of $248,000 amounts to about 397% of their disposable income. Overall, 44% of Gen X consumers have debts that surpass $250,000.

In comparison, bridge millennials and millennials owe about $220,000 and $204,000, respectively, and baby boomers and seniors of customers have outstanding debt balances of $174,500. Generation Z, on the other hand, have the least debt of $87,000.

The study identifies mortgages, auto loans, and credit cards as the primary contributors to consumers’ high debt levels, with almost all (97%) having mortgages, compared to only 26% of those with low debt.

Similarly, more than half of high-debt consumers have auto loans, while only 26% of low-debt consumers possess them. Additionally, 52% of high-debt consumers rely on store credit cards, in contrast to 38% of low-debt consumers.

Managing this high level of debt prudently is no doubt crucial, as mismanagement can lead to adverse consequences such as overdue payments, which 3 in 10 consumers have to grapple with.

Late fees associated with overdue payments have also become a cause for concern. The study estimates that American families pay a staggering $12 billion in late fees annually. In response, the U.S. Consumer Financial Protection Bureau (CFPB) has proposed reducing these fees, aiming to alleviate the financial burden on consumers.

To address the high levels of debt among consumers and Generation X consumers, in particular, a multifaceted approach is necessary. Regulatory interventions, such as reducing late fees, for instance, can provide immediate relief.

Additionally, more consumers can improve their financial management skills and credit scores through credit-building applications. The study reveals that 46% of high-debt consumers facing credit score issues have used credit-building apps in the past year, compared to only 7% of consumers without such issues.

Overall, the study’s findings underscore the urgent need for Generation X consumers to tackle their mounting debt burden.

By managing debt responsibly, enhancing financial literacy, and leveraging available resources like credit-building apps, these consumers can work towards reducing their debt and achieving better financial stability. Regulatory measures, such as reducing late fees, can further alleviate the strain on Generation X consumers and promote a healthier financial future for this age group.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More