Not so long ago, few people openly talked about their own personal finances or budget challenges. However, as noted earlier in May by The Wall Street Journal, younger consumers are changing this behavior and instead candidly airing their financial laundry. Included in this effort are TikTok videos in which creators go over their income and spending in minute detail. The popular hashtag #paydayroutine has 57 million views, as users seek tips and tricks to help them rise out of their paycheck-to-paycheck lifestyle.

This advice may be enjoying such high receptivity due to more than 60% of U.S. consumers living paycheck to paycheck, as illustrated in the May PYMNTS collaboration with LendingClub, “New Reality Check: The Paycheck-to-Paycheck Report.”

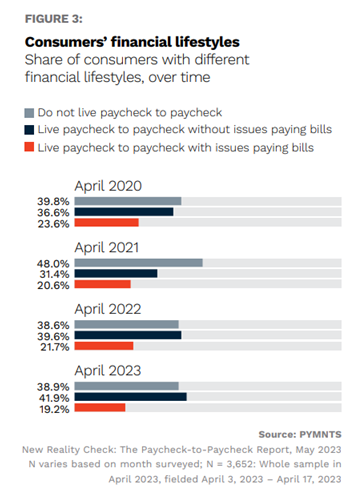

Here we see that the rate of consumers living paycheck to paycheck with issues paying bills is at its lowest in more than three years. This positive news, however, has been somewhat blunted by the reality that the share of consumers living paycheck-to-paycheck without issues paying bills, 42%, has reached a high point during the same period. Clearly, there is a significant share of consumers living under a notable level of financial stress.

Moreover, the popularity of personal finance chatter on social media indicates that a portion of these paycheck-to-paycheck consumers are actively looking to elevate their financial standing. This may represent a loyalty and retention opportunity for FIs targeting the consumer segment. Previous PYMNTS research has found that 44% of consumers with at least one credit card through their primary FI are very or extremely interested in payment recommendations for purchases from their banks. Additionally, younger consumers specifically show a strong preference for robust digital tools to help them manage their wealth on both sides of the Atlantic.

In an interview with PYMNTS, President and CEO of Metro Credit Union Robert Cashman explains how offering financial advice and other guidance may be a mutually beneficial relationship for both FIs and their customers.

“We know that when members feel engaged and prioritized, they remain loyal to a financial institution, so we are committed to providing the same consideration to them. Our members are our biggest asset, and we understand that they put a lot of trust in us, especially during difficult economic times.”

In these continuing trying times for the majority of consumers, some are actively seeking help managing their finances. And, as demonstrated, if FIs don’t provide this advice, they will go elsewhere.