As a result, a significant share of consumers continue to struggle with managing their finances — a challenge that fluctuates with the seasons, according to findings detailed in “New Reality Check: The Paycheck-to-Paycheck Report — The Seasonal Financial Distress Deep Dive Edition.”

The research study, produced in collaboration with LendingClub, draws on insights from a survey of over 4,200 U.S. consumers to assess the impact of seasonal spending on consumers’ ability to manage expenses and grow their savings.

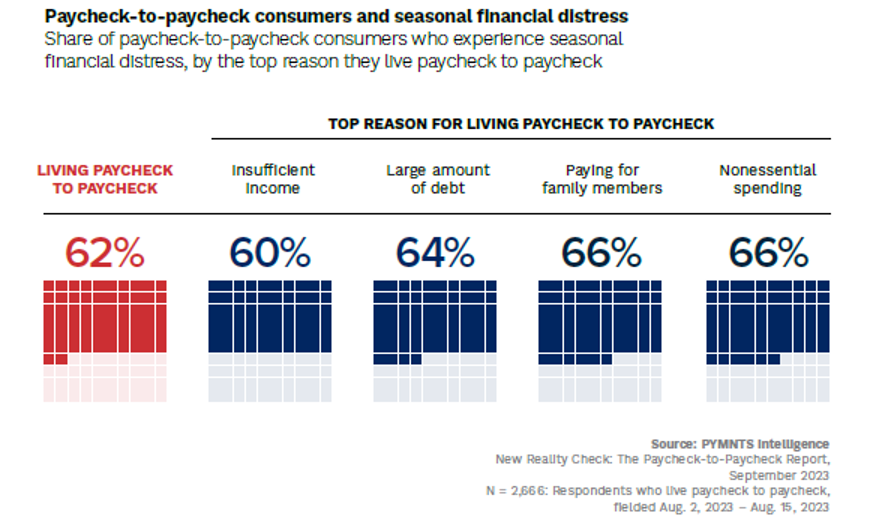

Per the report, one of the primary reasons cited by consumers for living paycheck to paycheck is nonessential spending. In fact, 66% of consumers engage in splurges and unnecessary purchases, which can strain their finances, and by doing so are more likely to experience significant fluctuations in their financial situation throughout the year.

Another significant factor contributing to living paycheck to paycheck is family financial support. Here too, 66% of consumers who provide financial assistance to their loved ones cite this as a top reason and may need to consider setting boundaries to avoid putting a strain on their own financial stability.

Having a large amount of debt and insufficient income are also cited as top reasons for living paycheck to paycheck by 64% and 60% of consumers, respectively. The study suggests that those who identify insufficient income as the main reason for their financial struggles are less likely to experience significant fluctuations in their financial situation throughout the year. However, it is important for these consumers to explore ways to increase their income or find alternative sources of financial support to enhance their overall financial stability.

Advertisement: Scroll to Continue

In conclusion, despite lower inflation rates, living paycheck to paycheck remains a prevalent challenge for most American consumers. The study emphasizes the impact of nonessential spending, family financial support, high debt, and insufficient income as key contributors, underscoring the importance of proactive steps to improve overall financial stability all year round.