Inflation, consumer cutbacks, and limited access to capital are all hindering small and medium businesses (SMBs), which are turning to digital tools to close gaps and firm up operations.

While throngs of shoppers returned to physical stores in 2022 and so far in 2023, they’re spending less and are less tolerant of clunky checkouts and lackluster digital shopping features found online and in enterprise retailers, which is adding to their pressures.

As found in The 2023 Global Digital Shopping Index: SMB Edition, (GDSI-SMB), a PYMNTS and Cybersource collaboration, 70% of all SMB customers across the six countries studied completed their most recent purchases at a brick-and-mortar store, but many report less satisfying shopping and payment experiences among SMBs, which calls for change.

Per the GDSI-SMB, “Consumers use mobile channels more often to shop and pay, but smaller merchants are missing the opportunity to capture those sales. Twenty-one percent more consumers shopped via smartphone year over year, and 32% fewer shopped via laptop, but SMBs are still 32% less likely than their larger competitors to provide mobile apps or mobile-specific sites.”

There’s a catch-22 at work as SMBs have a more difficult time accessing the working capital needed to license and install digital systems that would close experiential gaps.

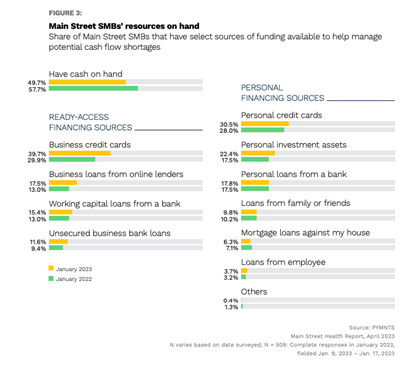

In the study, Main Street Health Q1 2023, a PYMNTS and Enigma collaboration, based on surveys of over 500 SMBs, only 26% of Main Street businesses across the U.S. have access to the equivalent of at least 60 days’ worth of revenue, and 17% have no ready access to emergency funding at all. Without that working capital cushion and growth capital, bettering checkout and the digital shopping experience is out of reach for a large portion of U.S. SMBs.

In this climate, we found SMBs looking for ready sources of working capital.

Per the Main Street Health Q1 2023 report: “Business credit cards are the most common financing option that Main Street SMB owners have for contingencies, with 40% saying they can finance their companies with business cards in case of a cash flow shortage. Meanwhile, the share of companies turning to business loans from online lenders, working capital loans from banks, and unsecured business loans is up 24%, on average, compared to last year.”

SMBs represent an opportunity for lenders, but banks and FinTechs in the working capital space have tightened up credit considerably. Some are connecting SMBs with willing lenders, which can go a long way to prevent Main Street business closures in 2023.

In a recent interview with PYMNTS’ Karen Webster, Rohit Mathur, head of Bridge built by Citi, explained that “There’s not many out there helping connect borrowers and lenders in the $250,000 to $10 million space,” adding that “we have 70-plus lenders, including community banks and CDFIs (Community Development Financial Institutions) focused on SMB lending that can help these clients.”

PYMNTS also analyzed the issue in the report Digital Banking Rises To Meet SMB Needs, an NCR collaboration. It noted that 75% of SMBs seeking working capital are the most likely to use a digital-only bank as their primary financial institute (FI) in this business lending climate.

According to that report, “The pressure to find the right working capital solution is increasing, with one survey finding that big banks’ approval rate for business loans dipped to just below 15%, a 10-month low. Alternative lending saw the biggest increase at nearly 2%, meaning small businesses are increasingly looking to FinTechs and digital-first offerings to deal with cost pressures.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More