There’s the promise, and then there’s the peril.

Special purpose acquisition companies (SPACs) were heralded not all that long ago as streamlined ways to take innovative companies — particularly tech companies — public.

And now comes the reality check. The same factors that separate these so-called “blank check” firms from traditional initial public offerings (IPO) are proving to be headwinds, so much so that the SPAC model itself is being put to a test on Wall Street that seemed far-fetched once upon a time.

Amid the continued whipsaw that is the stock market today, the Wall Street Journal reported Wednesday (May 18) that SPACS are “running out of time” to buy the firms they need to buy and take those targets public, which, we note means that they may have to unwind and return cash to investors.

The dearth of deal-making is a dagger at the heart of the SPAC itself — where the underlying business is predicated on merging with another company. The mechanics are such that a shell company takes shape, with some funding (from investors) and then goes on the hunt to buy a promising, typically young firm, within a timeframe that lasts two years.

Advertisement: Scroll to Continue

Along the way, there are all sorts of projections, estimations of markets and competitive dynamics within the SPAC’s chosen vertical and its targeted firm. The projections? Well, they can be as rosy as can be — and tend to be quite a bit sunnier than what we normally see with the U.S. Securities and Exchange Commission disclosures that are part and parcel of the traditional IPO process.

In the meantime, companies that have been taken public via SPAC such as DraftKings are down more than 50% in recent months, outpacing the declines seen in the tech-heavy NASDAQ, which is off more than 25% year to date.

Time is Running Out

The Journal noted that roughly 230 SPACs have to get a deal done by the first quarter of 2023 — so time is running short, against a backdrop where 90% of SPACs stretching back to 2020 are essentially trading as busted IPOs.

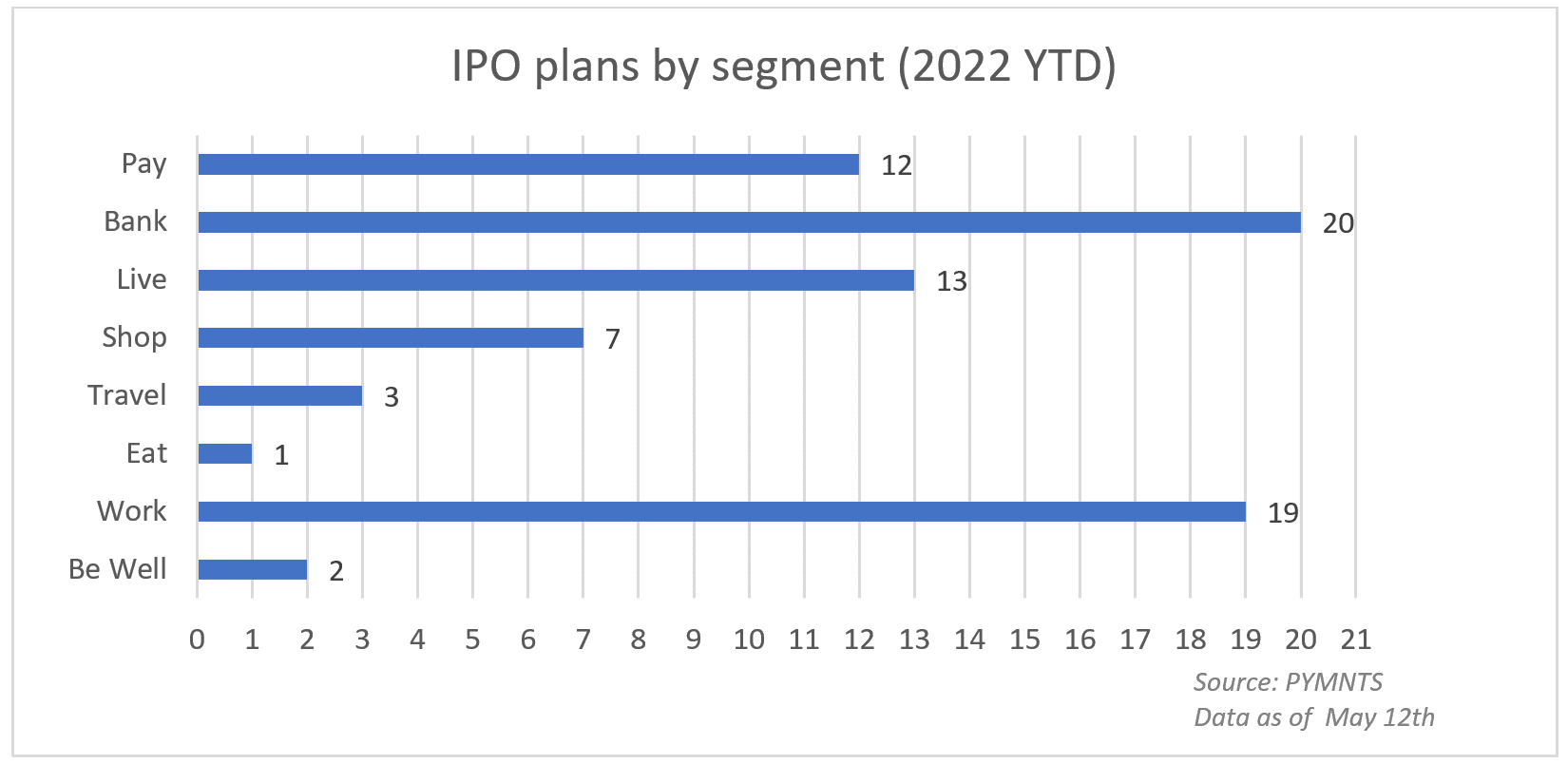

PYMNTS’ own data spotlights the dwindling enthusiasm for SPACs, and for IPOs in general, across the pillars that define the connected economy and which are tied intimately to the great digital shift. For just a few illustrations, consider the fact that year to date — and we’re almost halfway through the year, payment-related announced listings stand at 12; through all of last year, that segment had logged 40 listings announcements. The “shop” pillar has thus far seen 7 listings, paling before the 22 that had been seen in all of last year.

You get the picture. Investors — particularly the institutional ones, are waiting on the sidelines.

But even upon coming public — well, that’s where some real trouble can brew. As we noted in this space recently, the FinTech IPO Index, a separate tracker that includes names that have gone public over the past two years (with SPACS among them) has been hitting fresh lows. The year-to-date loss is more than 50% for that Index.

That’s enough, we’d think, to give the blank check companies sitting on the sidelines, flush with cash an excuse to remain on the sidelines. Runaway inflation and rising interest rates raise the bar for investors’ returns.

For SPACs all of a sudden, the wait-and-see approach — waiting for the right takeout target — turns eventually into a race against the clock, or they’ll have to give up the money that once seemed so easy to raise.

Read Also: Plummeting FinTech IPO Index Carries Warning for Future Startup Funding