Subscription services are hot, yet some industries have embraced subscriptions better than others. One of the segments facing more of a challenge is consulting and financial services, according to the Subscription Commerce Conversion Index.

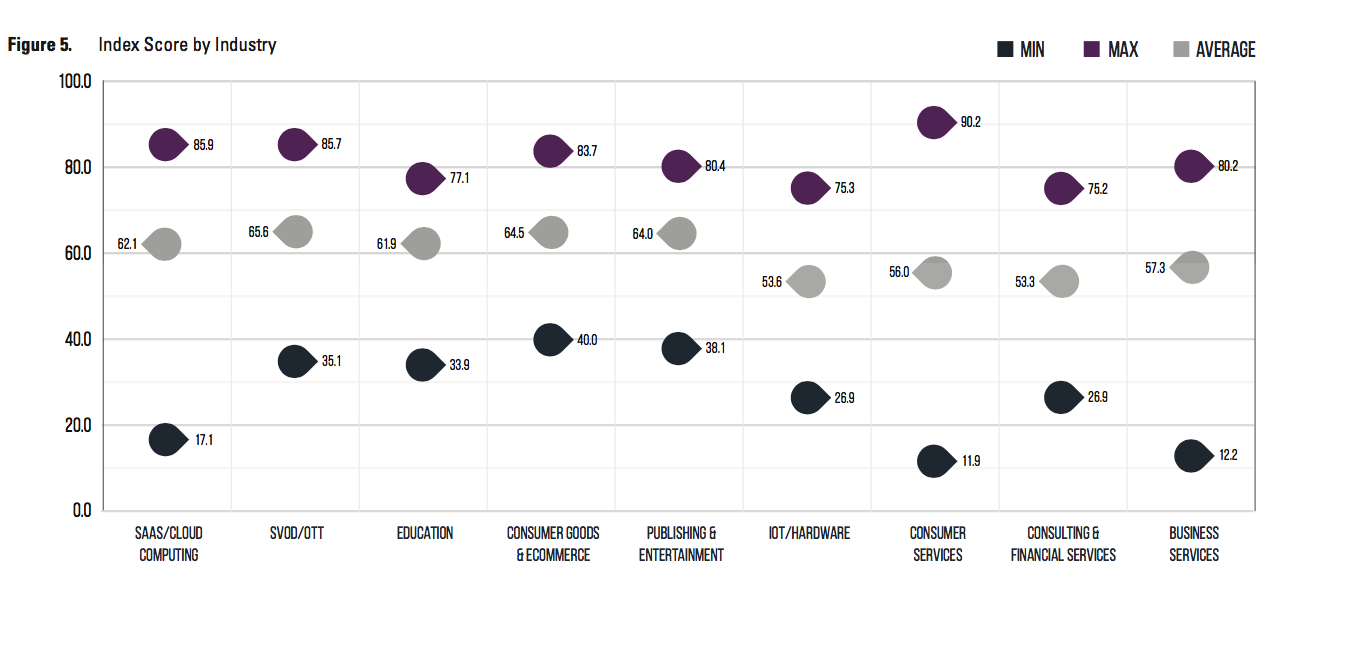

In the most recent quarter, the industry had the lowest score among the nine industries the PYMNTS study analyzes, with a 53.3 mark out of 100. By contrast, streaming video and on demand (SVODD/OTT) services averaged 65.6, highest among all industries. Even those financial services companies that outpace their peers still lag the best of breed in other segments, posting a top score of 75.2 in the latest SCCI report. None of the SCCI top 20 companies were from financial services.

Part of the challenge for the sector is that often subscriptions are simply viewed as fees in the eyes of consumers, especially millennials, writes digital commerce consultant Jim Van Dyke in American Banker. Even when banks look to charge for services, customer resistance means financial services are charging too little to really improve the subscription services they offer, Van Dyke wrote.

Bank of America is a large institution that has repeatedly faced this problem, for example, facing protests and threats of boycotts over debit and checking account subscriptions that offer only incremental value, such as overdraft protection features. And research shows consumers are quick to leave subscriptions that have a lack of perceived value, according to a McKinsey & Co. white paper.

The key, then, is to offer subscriptions that break new ground, rather than offer a slight improvement on previously free services. For example, micro-investing app Acorns has rolled out Acorns Later, an automatic retirement plan with value-add services such as initial account size minimums of just $5 and the ability to set recurring contributions by day, week or month. The service also offer automatic rebalancing and access, in regular Acorns, to portfolios designed by Nobel Prize winner Harry Markowitz and others. The subscription starts at $2 a month. “Acorns Later removes friction from the decision making process, getting back to our central product philosophy: Make big decisions small,” Acorns CEO Noah Kerner said.

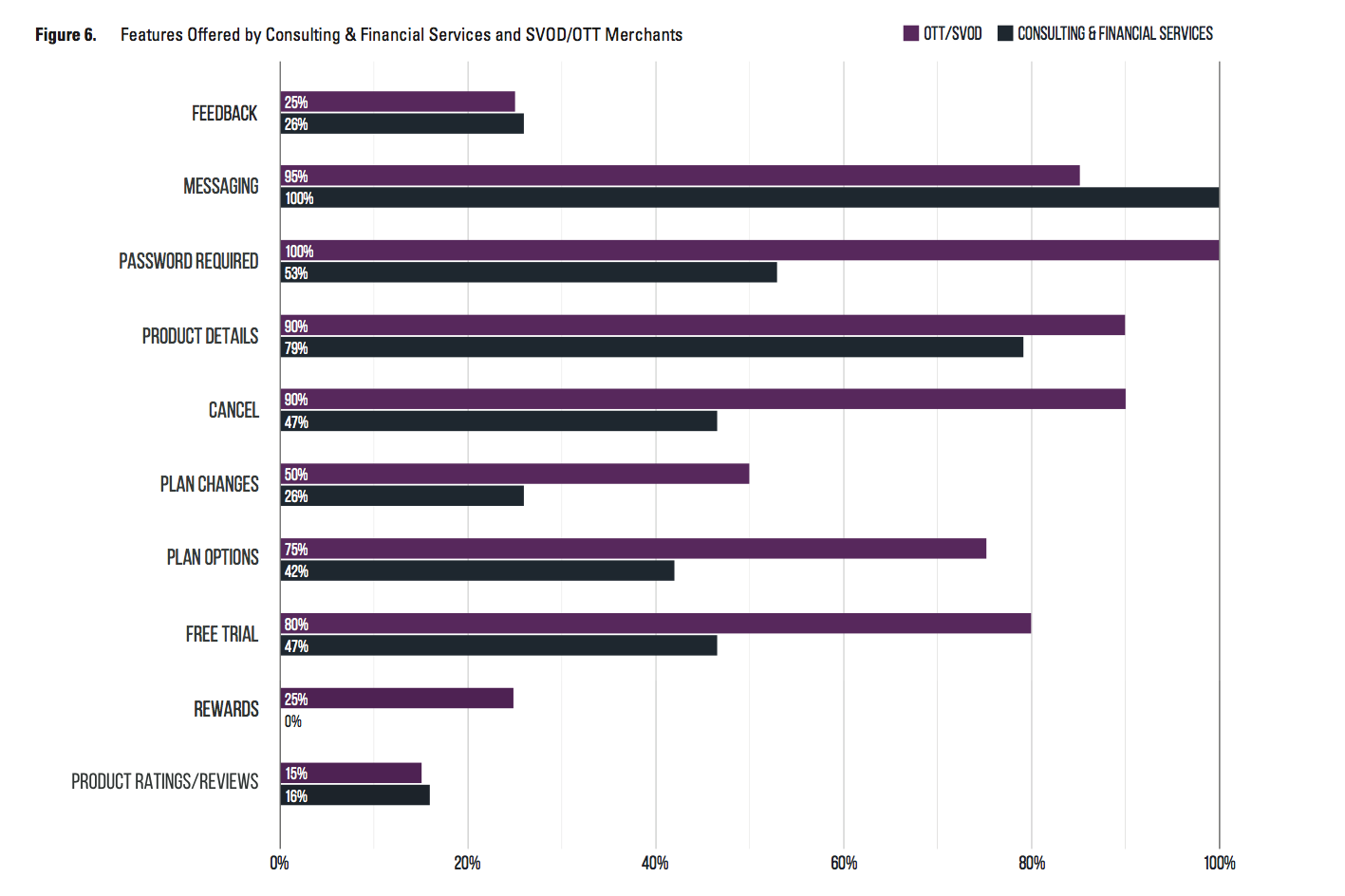

One of the features Acorns offers is the ability to cancel at anytime. The findings of the Subscription Commerce Conversion Index show that this is an area where financial services as a whole lags. Just 47 percent of companies analyzed offer cancel anytime. That’s three points behind the next worst sector, Internet of Things/Hardware, and a wide 43 percentage points behind the leading sector, SVOD/ITT.

Advertisement: Scroll to Continue

Financial Services do perform well in some areas. Every consulting and financial services company subscription examined in the latest quarter offer messaging services and has password requirements implemented, two metrics measured by the SCCI. Fully 90 percent of financial services firms score well on product details. Each of these outpaces the average of subscriptions services overall.

Subscriptions also benefit financial services companies when they allow access to services that previously required a high minimum investment of assets or a high consulting fee. Life planning – for a family, retirement and the like — is one prime example. It’s an area where customers traditionally have had to pay a percentage of their assets as a fee quarterly or annually, regardless of performance. The result is that there is a gap between customers who would use the service if they believed they could afford it and those who actually use a financial advisor.

In a discussion of how advisors structure their subscription fees, Financial Advisor magazine noted a statistic from the Economist Intelligence Unit that 80 percent of consumers want alternatives to buying a product or service outright. The sector still has some work to do in that area, however, with 47 percent of companies offering free trials and free cancellation, according to the SCCI report. Subscriptions also have the benefit of removing some of the inherent conflict in advising a client based on assets under management or in which billing is based on actual hours of work.

“It creates a feeling of trust; I’m someone who will be with them as their lives evolve and they need to make the best decisions they can for themselves and their families,” Cristina Guglielmetti, president of Future Perfect Planning, told Investopedia.