The retail subscription sector is feeling the pain of financially tapped-out consumers or those simply disenchanted with the workings of subscription plans, making retention strategies and increasing lifetime value (LTV) the mission for subscription merchants in the second half of 2023.

This effect is evident in new research that examines the personas of subscribers and gauges their plans for keeping — or cutting — some of their subscriptions in the coming months.

Looking at “The Subscription Commerce Readiness Report: The Loyalty Factor,” a PYMNTS and sticky.io collaboration, based on a survey of nearly 2,100 U.S. consumers, a slight uptick of 0.2% in retail subscriptions between February and April didn’t make up for the drops between of 3 percentage points among high-income consumers and 3.8 percentage points among millennials observed during the same period.

That gives the first quarter of 2023 the dubious distinction of consumers holding the lowest recorded number of subscriptions per subscriber since February 2021, averaging just 2.6 subscriptions each.

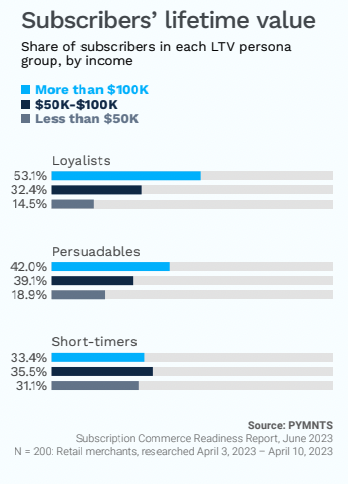

Separating the primary subscriber personas as “loyalists” who spend an average of $65 a month on retail subscriptions, “persuadables” who average a $42 monthly spend, and “short-timers” who spend $30 per month, it’s the loyalist group with an LTV averaging 30 months that subscription merchants need to build on by pumping up features and retention strategies.

A good place to focus efforts is on persuadables — the clue is in the moniker — as they can be swayed by the right offer and feature set, allowing merchants to convert a chunk of this group into loyalists using a combination of products, price and feature set.

“Consumer expectations of subscription experiences are more refined than ever, emphasizing the value of free shipping and flexible subscription policies and features,” the study found. “These features have become table stakes for acquiring and retaining subscribers. Free shipping is the most valuable feature, with 39% of consumers shopping for a subscription plan naming it as their top requirement.”

Digging into the numbers, we see the promise of persuadables in a few ways. Those making $100,000 a year have a shorter LTV than loyalists. However, persuadables earning $50,000 to $100,000 have an LTV of 39.1% compared to 32.4% among loyalists, suggesting that more of the former group can be converted to lucrative loyalists if merchants tailor offerings accordingly.

An instructional use case in turning more persuadables into loyalists can be found in Amazon Subscribe & Save.

“Unlike other subscription services, Subscribe & Save allows subscribers to commit to specific products, offering a level of choice currently unmatched in the retail subscription space,” the study stated. “It also grants subscribers the freedom to adjust the frequency of their plans or suspend their subscriptions per product at any time without penalty.”

The power of free shipping can’t be understated with 39% of respondents across the spectrum calling it the most valuable feature they look for when signing up for a retail subscription plan. It’s followed closely by flexibility, with 31% of respondents naming a free and flexible cancellation policy as their top preference, and 20% naming the ability to change subscription frequency as their most preferred feature. It’s information that can inform the roadmap of subscription merchants that focus on retention and LTV in their strategies.

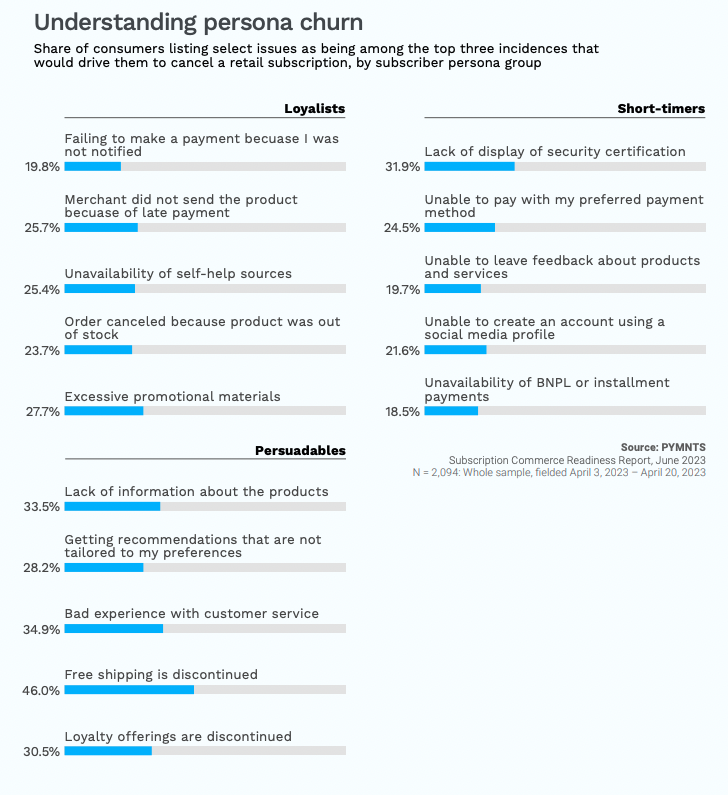

Another key is transparency in the renewal process, as 32% of subscribers “identify the absence of explicit renewal notification as a potential reason for cancellation. We estimate that this subset of customers has a higher-than-average LTV at $2,492, meaning that providers risk losing especially lucrative subscribers simply by neglecting to ask about renewal preferences.”

Top-performing merchants have cracked the code on loyalty and LTV, reducing churn by keeping subscribers happy and feeling in control of their subscription assortment.

Per the study, 93% of top-performing merchants provide free shipping compared to 76% of middle performers and 37% of bottom performers. Subscription pause is used by fully 100% of top-performing merchants versus 71% and 23% of middle- and bottom-performing merchants.

“Seamless sign-up via social media or similar accounts has become the norm among top performers, with 67% now offering this feature,” the study found. “No bottom-performing merchant and just a small portion of their middle-tier peers provide this feature.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More